Law #1 – Business Return Determine Investor Return

This goes back to the first principles of investing: a share in hand is the same as owning a fraction of the underlying business. When you own a company’s share for 10, 20, or 30 years, your return will be similar to the return of the business.

In the short term—a month to a year—your return is likely to be different from the business return due to changes in market sentiment and expectations. But as the time horizon stretches out over 10 years or more, all the market volatility gets washed away. Just as if you look at a stock’s 30 days price chart, you’ll observe all the zig-zagging in every imaginable pattern. But switch it to a 10 years price chart, all the volatility would give way to a much smoother terrain that reflects the business’s long-term return.

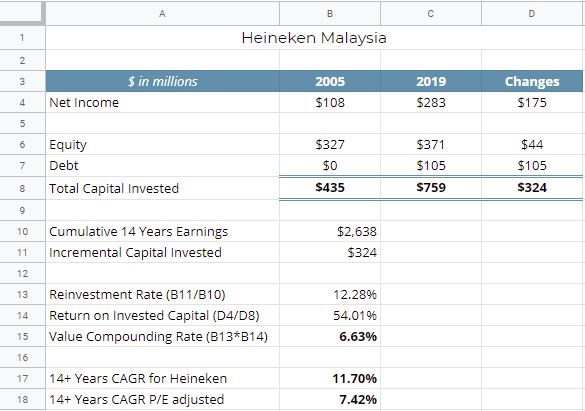

Take Heineken listed in Malaysia as an example. Over the past 14 years, Heineken invested $324 million into the business, roughly 12% reinvestment rate; the rest is paid out as dividends. And with a return on invested capital of 54%, the business’s intrinsic value would compound at 6.63% annually (ROIC x Reinvestment rate). During this period, Heineken’s share price has compounded at almost double the rate—12% p.a. The reason is that the P/E ratio has expanded from 15x to 26x. Had it remain unchanged, the CAGR would be 7.42%, tracking closely to 6.63% p.a value compounding rate.

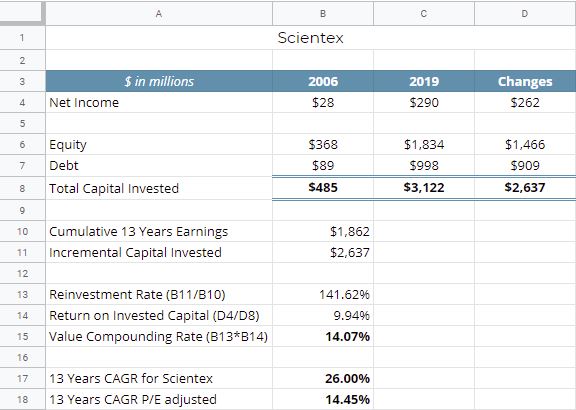

Let’s apply this to a stock I own, Scientex. Scientex’s ROIC of 10% looks relatively poor compared to Heineken’s 54% return but managed to compound its value at 14% over the past 13 years, double of Heineken. The reason comes down to its reinvestment rate. Scientex has more reinvestment opportunities (partly using debt) compared to Heineken where the growth opportunity is limited. Again, Scientex’s share price has compounded at 26% during this period, but when P/E gets adjusted, the share price return mimics the intrinsic value compounding rate of 14%.

Law #2 – Price Determine Return

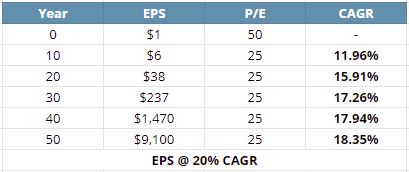

We can deduce from the first law that how much you pay for a stock affects your long-term return, but not as much as you think. Consider a business that can compound its earnings per share at 20% for the next 50 years. If you pay 50x for the stock today and sold it at 25x 10 years later, your return will be 12%, roughly half of the business’s return. But your return eventually ‘catches up’ to the business return when the holding period stretches to 30-50 years.

A 50% change in the P/E is an extreme case. So even if you slightly overpaid in the initial purchase, you should still do fine over the long-term, provided you bet on the right horse. Of course, no one can predict what’s going to happen in the next 10 years, much less so for anything beyond that. And add to the fact that we are always overconfident in our judgment, having a margin of safety on the price you pay is prudent advice.

Law #3 – Capital Allocation Affects Return

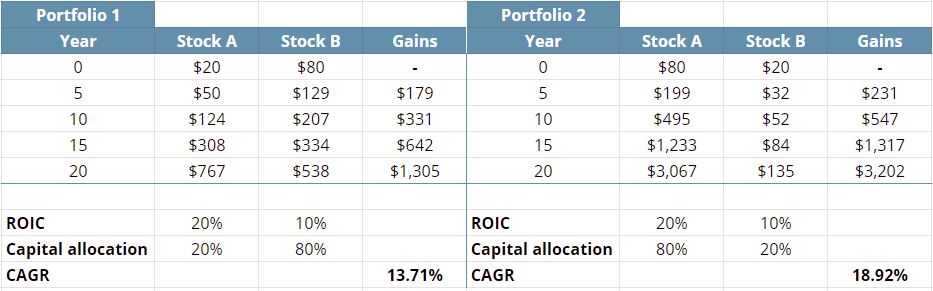

How you allocate your money determines your long term return. Imagine two portfolios where in the first portfolio, an investor allocate 20% capital to Stock A that compounds at 20% and 80% capital to Stock B that compounds at 10%; the second portfolio has the opposite: 80% capital on Stock A and 20% on Stock B.

At year 5, the 2nd portfolio would outperform the 1st portfolio by 29%; year 10, 65%; year 15, 105%; and year 20, 145%. In real life, we don’t own only 2 stocks, of course. But this example illustrates that position sizing is as important as picking the right stock.

For every dollar in hand, you want to allocate that dollar to ‘maximize’ your long-term return. And following law #1, your long-term return will be the weighted average of all the stocks’ business returns in your portfolio.

Law #4 – Compounding Magnify Return

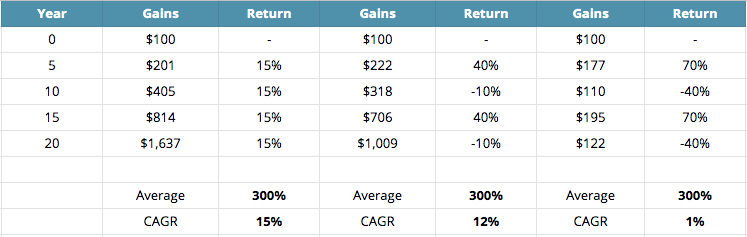

All the laws above sit on the most important law: compounding. The precondition of compounding is to avoid big losses since avoiding losses is paramount to the preservation of capital.

To illustrate, assume there are 3 investors, whose yearly return differs from one another but on average, their investment returned 300% over the past 20 years. Their outcome should be the same right? No. The investor that can generate a 15% return consistently is going to beat the one that makes an alternating 40% gain and 10% losses, who again, will outperform the one that alternates between a massive 70% gains and 40% losses. Investing is non-ergodic. History matters in the context of investing. Your starting point determines where you end up with.

No one can control their annual investment return, of course. But the emphasis here is that it is better to avoid big losses than to miss out on big gains. Investing is about managing risk. The margin of safety should not be a substitute when the risk of permanent loss of capital is almost certain.

Law #5 – Decisions Dictates Return

Every decision you make: what to buy or sell, when to buy or sell, how much to allocate etc, directly influence your long-term return. And how you make these decisions depends on the quality of your thinking. This seems evident, but our actions often tell a different story. Most investors spend their time on why the market or a certain stock is going down, how the share price is doing, what’s going to happen to the price etc. These are things outside our control where the odds of getting it right consistently is as good as winning the lottery (which is less likely than getting hit by lighting). Not to mention the risk of losses is almost certain.

On this point, my boring advice remains the same: focus on what you can control and things that are not going to change. If how you think determines how you make decisions, then pay attention to how you think. And since the way we think is heavily influenced by all sorts of psychological factors, you’ll want to understand those things so you reduce your biases and misjudgment, which is the essence of having a good investment process.