“We are trying to prove ourselves wrong as quickly as possible, because only in that way can we find progress.” – Richard Feynman

Investing is part art, part science. There’s no single formula for success as the future is uncertain, probabilistic, and constantly changing (our forecast changes the outcome). All of which rely on our judgment to get it right. That’s the art part. But it is not all art. Otherwise, investing will be as good as astrology. The science part is about a systematic approach to ‘get it right’ to improve the accuracy of our judgment so we are less wrong. And the only way you can get as close to the ‘truth’ as possible is to first, kill your ideas.

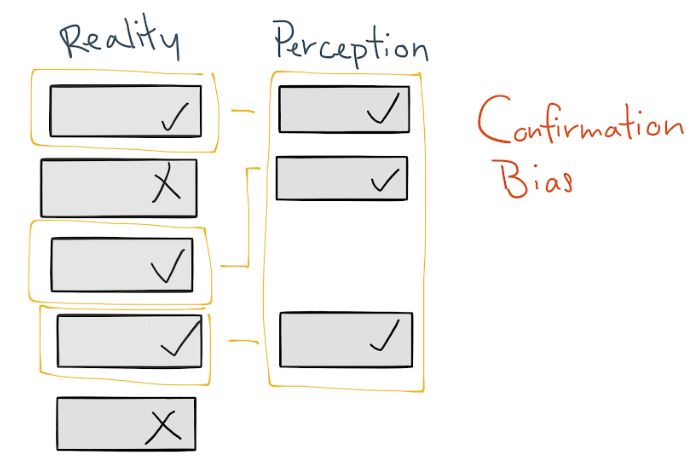

Confirmation bias

We perceive what we want to perceive. Just as how we like someone we never met before, we tend to fall in love with our investment ideas before analyzing. This halo effect nudges us to only collect information that supports our preconceptions and ignores those that contradict.

A common scenario is a stock that appears in the news or social media because of bullish market sentiment and a surging share price. After reading a few write-ups that confirms the stock’s future potential, you did your own ‘research’ and conclude that it is an attractive investment despite the risks involved.

There is a difference between analysis during data collection and analysis after data collection. If you analyze a piece of information as you collect it, that perception is likely to lead you to collect the next piece of information that confirms with the prior information. As a result, the analytical process becomes path dependence: A favorable perception on a piece of information leads to the finding of another favorable piece of information ad infinitum. Contradictory information that is found along the way either gets ignored or forgotten. Then there is information asymmetry.

No one talks about a stock that they didn’t end up buying. Therefore, you are more likely to find information on why you should buy than why you shouldn’t buy it. If 10 out of 100 people think a stock is a great buy, 5 (out of 10) will share their opinions. What you don’t hear are the opinions of the other 90 people. This silent evidence is more important.

Confirmation bias acts like a distortion field that wraps our mind in a bubble, unable to see what is out there. While having false beliefs in life is harmless most of the time, it can have disastrous consequences in investing. You are likely to become overconfidence that leads to misjudgment— overestimate potential gain and underestimate actual risk—both contribute to immeasurable risk-taking and massive losses.

Falsification

How do we counter this bias? How can we be more right and less wrong? Karl Popper, one of the 20th century’s greatest philosophers of science, offers a clue. He once explains falsification, “No amount of observations of white swans can allow the inference that all swans are white, but the observation of a single black swan is sufficient to refute that conclusion.”

The quickest way to validate an idea, a theory, or a hypothesis is not to confirm, but to falsify it. Let’s say you notice many successful people are early risers who wakes up before 6 am. So there must be a causal relationship between waking up early and being successful. But how do you know the hypothesis of waking up early increases your chance of being successful is true? Common sense would tell you to find more confirming evidence to strengthen this belief. But no amount of confirming evidence can prove this to be true. In contrast, single evidence of an early riser that never succeeds is enough to reject this hypothesis.

We are constantly making causal inferences in life to make better predictions. That’s the same in investing. Let’s say you have an idea that the steel price is going to increase in the near term due to regulation and tight supply. Therefore, you postulate that earnings for steel-related stocks are going to do well, and the share price should go up. In a way, you’re saying an increase in earnings will be positive to the share price. Now you can easily back up this belief with many confirming information. But these confirmations can be destroyed by finding instances where an increase in earnings has an opposite effect—a drop in price.

Asymmetrical return

Falsification or killing ideas is a shortcut to get to the truth. This approach has two advantages: opportunity cost and asymmetrical return.

The time spent on one stock means less time for other stocks. There is a huge opportunity cost to spend countless hours on a promising idea that turns out to be a lemon. Those precious time could have been used on other worthy investable ideas. Hence, you want to spend more time with high potential, high probability stocks compared to ones that you think it is but aren’t. And the quickest way to separate good opportunities from lemons is to refute it.

The main point of killing ideas is this: it is more important to avoid bad ideas than finding good ones. Besides, it’s also easier to do the former than the latter. Investing is about managing risk; look after the downside, and the upside takes care of itself. The faster you can get rid of bad ideas, the lower the chance of losses. And not losing money, especially big losses, is the key ingredient that makes compounding possible.

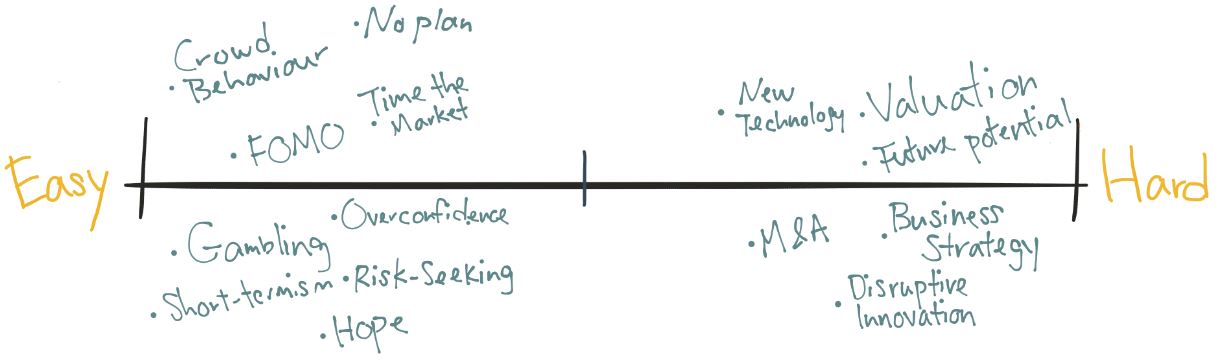

Degree of killability

Not all ideas are equal. You can think of a spectrum where some ideas are easy to kill, while some are not as straightforward. If your idea is a stock that can double its revenue over the next 3 years, apart from assigning a probability of that happening, it cannot be dismissed entirely because the future has yet to happen. So anything that involves future uncertainty such as growth strategy, new products or technology rollout, disruptive innovation, etc falls under the ‘hard to kill’ side.

Ideas that fall on the ‘easy to kill’ side tend to be psychological, ideas born out of crowd behavior, overconfidence, short-termism, etc. This is where we should focus most of our energy on because of asymmetrical payoff: ideas that are the easiest to kill are investment mistakes that produce the biggest losses.

Think for a second, what are some ideas that can be refuted in a split second? They are a castle in the sky ideas produced in the cloud of euphoria. They are the easiest to kill through self-control, second-level thinking, and simple tools like a checklist. Investment mistakes follow a power law: 80% of the losses come from 20% of the mistakes. Most of these mistakes don’t come from the failure to predict the unknowable—what would happen in 10 years—but from the failure to manage the preventable, tiny mistakes that snowball into catastrophic losses. Therefore, focus on avoiding these easy-to-kill mistakes would improve return exponentially by eliminating 80% of the losses.

Stress test

Trying to kill ‘hard to kill’ ideas has its benefits as well. Killing ideas is negative thinking. You ‘stress test’ your ideas under various economic conditions to find out under what circumstances will they fall apart. If your idea relies on a 15% growth assumption, what will prevent that from happening? What if the demand goes from 8% to 5%? What if the competitors lower their selling price in an oversupply situation? What if there is a supply constraint on raw materials? The answer to most of these questions is unknowable. But the value isn’t so much about having the answers, rather, it lies in the thinking process of what can go wrong so you have a plan B, C, and D to handle them.

Killing your ideas is like planting minefield flags. You develop a strong pattern recognition as if you’re planting minefield flags along all the dangerous pathways. And you’ll be prepared if a situation unfolds ever closer to those flags. One of investing’s powerful thinking tools is when the facts change, change your mind—strong opinions, weakly held. That is, it’s okay to have a strong conviction, but be ready to discard it when the condition changes. How do you cultivate the ability to hold opinions weakly? Or in other words, how do you know when does experience started to betray instead of helping you? You learn that by killing your ideas. Instead of having a closed attitude, killing ideas create open-mindedness because it allows you to see the boundaries of your ideas, know what you don’t know, and be ever ready to abandon your plan when it becomes irrelevant.

Position sizing

Another natural outcome of idea killing is that you develop a good judgment on the durability of each idea. Think of ideas as clothes inside a wardrobe; some clothes are only suitable for specific occasions, while others are everyday clothes that can be worn over a wide range of occasions. Just as it makes sense to have more everyday clothes than occasion-specific clothes in the wardrobe, ideas that can survive under various adverse conditions should have a higher portfolio weighting than ones that only work under a specific condition. These hard-to-kill investment ideas have a large margin of safety due to their ‘heads I win, tails I breakeven’ characteristics.

Evolution

Over the decades, antibiotic overuse on both human and livestock have created superbugs—bacteria resistant to the most powerful antibiotic. Every time you take antibiotics after falling sick, most bacteria gets killed, but some would evolve to develop resistance, multiply, jump to other people, and share their genes with other bacteria colonies. As this survival of the fittest process plays out over eon of time, superbugs acquire the potency that makes them deadlier than cancer.

If we replace ‘bacteria’ with ‘ideas’ and ‘antibiotic’ with ‘contradictory information’, evolution can teach us something about good thinking. Every time you expose your ideas to contradictory information by the way of trying to kill them, you speed up the evolution of your ideas. Similar to bacteria, weak ideas get eliminated in the process, while robust ideas that survive proliferate and replace the old thinking. It is through these continuous cycles of elimination process that improves the overall fitness of your ideas.

Randomness

Or consider the antifragile theory which explains that a certain amount of exposure to randomness reduces fragility. For example, a small dose of stress makes you more productive; some physical exercise is healthy for the bones, or a localized forest burning reduces the chance of a global scale firestorm. We can also think of how ideas become fragile when they get protected by supporting evidence. They become susceptible to shock similar to throwing a person into the wilderness for the first time. You want your ideas to be grounded on a solid foundation instead of a house of cards, and the only way to achieve that is to expose them to randomness—contradictory information. Always be ready to ask “What do I need to see to change my mind?” The defining quality of your judgment depends on your ability to kill your ideas as fast as possible. And every incremental progress that you make so your ideas become ‘more right, less wrong’ would determine the long-term investment outcome.

Notes

Taleb, Naleb. (2014). Antifragile: Things that Gains from Disorder: Random House Trade Paperbacks

Popper, Karl. (2002). Conjectures and Refutations: The Growth of Scientific Knowledge: Routledge

Yeo, Ricky. Why Negative Thinking Makes You A Better Investor. Apr 2019. https://musingzebra.com//why-negative-thinking-makes-you-a-better-investor/